SMM Alumina Morning Comment on June 23

Futures Market:Overnight, the most-traded alumina ag2509 futures contract opened at 2,900 yuan/mt, with a high of 2,925 yuan/mt, a low of 2,896 yuan/mt, and closed at 2,918 yuan/mt, up 12 yuan/mt or 0.41%, with an open interest of 293,000 lots.

Ore Aspect:As of June 23, the SMM Import Bauxite Index was reported at $74.41/mt, down $0.02/mt from the previous trading day. The SMM Guinea Bauxite CIF average price was reported at $74.5/mt, unchanged from the previous trading day. The SMM Australia Low-Temperature Bauxite CIF average price was reported at $70/mt, unchanged from the previous trading day. The SMM Australia High-Temperature Bauxite CIF average price was reported at $61/mt, unchanged from the previous trading day.

Industry News:

(1) Would a blockade of the Strait of Hormuz affect bauxite and alumina? According to SMM analysis, the impact on China is expected to be limited. China imports little bauxite via the Strait of Hormuz. China exports a small amount of alumina to the Middle East, but the volume is relatively small, totaling around 150,000 mt from January to May 2025, accounting for 13% of total exports. If the Strait of Hormuz is blocked, it is expected to affect alumina and bauxite imports to the Middle East. The blockade may cause crude oil prices to rise, driving up ocean freight rates for bauxite and alumina. However, the impact on long-term contracted shipping prices for Guinea bauxite is expected to be limited, while spot shipping freight rates may be affected, with limited upside for bauxite prices. Some market participants assess that the probability of a blockade of the Strait of Hormuz is low, and it is expected to have little substantive impact on the market. According to SMM, starting from June 20, a large alumina refinery in Shandong adjusted the purchase price of 32% ionic membrane liquid caustic soda, reducing it by 20 yuan/mt from the base price of 800 yuan/mt. The ex-factory price under the two-invoice system was implemented at 780 yuan/mt (approximately 2,438 yuan/mt converted to 100% concentration).

(2) A large alumina refinery in Shandong reduces the purchase price of liquid caustic soda: According to SMM, starting from June 21, a large alumina refinery in Shandong adjusted the purchase price of 32% ionic membrane liquid caustic soda, reducing it by 20 yuan/mt from the base price of 780 yuan/mt. The ex-factory price under the two-invoice system was implemented at 760 yuan/mt (approximately 2,375 yuan/mt converted to 100% concentration).

(3) Overseas alumina transactions: On June 20, 30,000 mt of alumina was traded overseas at a transaction price of $366/mt FOB India.

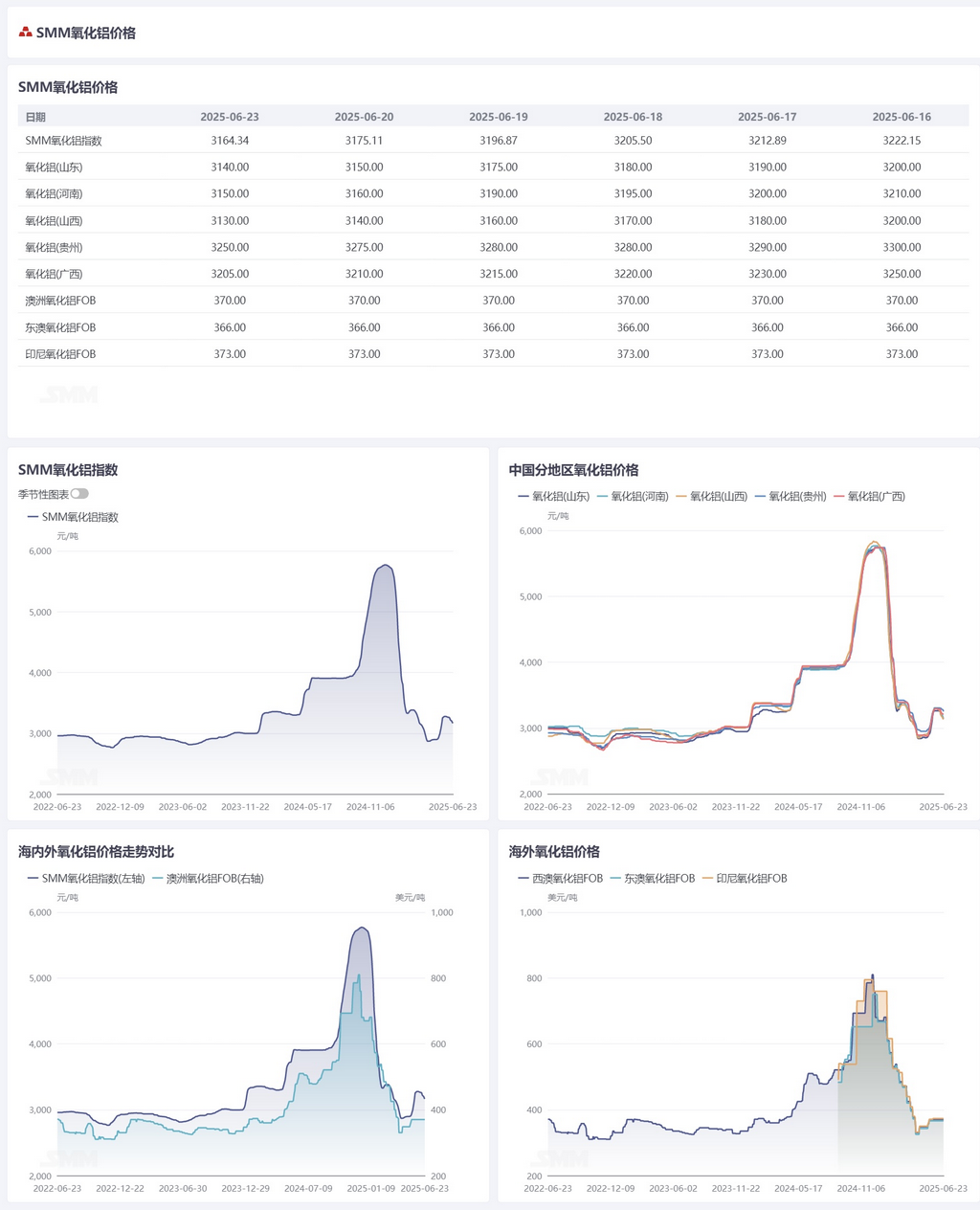

Spot-Futures Price Spread Daily Report:According to SMM data, on June 23, the SMM Alumina Index was at a premium of 273.34 yuan/mt against the latest transaction price of the most-traded contract at 11:30.

Warrant Daily Report:On June 23, the total registered volume of alumina warrants decreased by 5,394 mt from the previous trading day to 37,500 mt. The total registered volume of alumina warrants in the Shandong region remained unchanged at 0 mt from the previous trading day. The total registered volume of alumina warrants in the Henan region remained unchanged at 0 mt from the previous trading day. The total registered volume of alumina warrants in the Guangxi region remained unchanged at 2,701 mt from the previous trading day. The total registered volume of alumina warrants in the Gansu region remained unchanged at 0 mt from the previous trading day. The total registered volume of alumina warrants in the Xinjiang region decreased by 5,394 mt from the previous trading day to 37,500 mt.

Overseas Market: As of June 23, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $22.6/mt. The USD/CNY selling rate hovered around 7.2. This price translates to approximately 3,276 yuan/mt for the external selling price at major domestic ports, which is 111.18 yuan/mt higher than the domestic alumina price. The alumina import window remained closed.

Summary:

Last week, some alumina refineries completed maintenance and resumed production. Meanwhile, considering ore costs, there were reports of new production cuts. The operating capacity of alumina refineries experienced both increases and decreases. Overall, the operating capacity of alumina refineries decreased by 440,000 mt/year MoM to 88.57 million mt/year last week. Spot alumina supply remained loose. Last week, the total inventory of alumina at aluminum smelters increased by 8,600 mt to 2.655 million mt. In the short term, the alumina market fundamentals are expected to remain relatively loose, and spot alumina prices are expected to drop back slightly. Yesterday, the futures market fluctuated upward in the morning session due to news of the blockade of the Strait of Hormuz. However, after assessing that it would not temporarily affect the supply of imported ore to China, the futures market pulled back. Going forward, it is necessary to continuously monitor changes in the operating capacity and profitability of domestic alumina enterprises.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make prudent decisions and should not rely on this information to replace their own independent judgment. Any decisions made by clients are not related to SMM.]